While getting a home loan for a property under construction, you are given an option to choose between paying pre-EMI or full EMI. The pre-EMI option allows you to only pay monthly interest on the actual disbursed loan amount, with no principal repayment. The full repayment begins only when you take possession of the property. On the other hand, the regular EMI option allows the borrower to pay the full EMI from the beginning of the loan tenure even when the property is under construction.

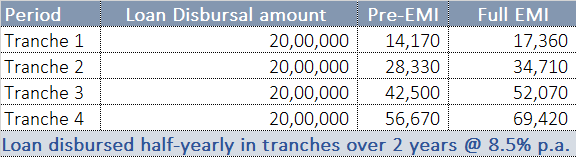

Let us assume you are availing a home loan of Rs.80 lakh at an interest rate of 8.5 per cent per annum for a tenure of 20 years. The property’s construction is expected to be completed in 2 years. The home loan will be disbursed in 4 tranches during the construction phase – of Rs.20 lakh every 6 months over 2 years.

Here is what you will pay if you choose the pre-EMI vis-a-vis the regular EMI option:

In the first tranche, your Pre-EMI will be Rs.14,170 which will go up to Rs.28,330 in the second tranche. From the third tranche, it will rise to Rs.42,500 and further climb to Rs.56,670 in the final tranche.

As you can observe from the table, pre-EMI is lighter on the pocket compared to the regular EMI as the outgo is only towards interest payments. It helps to manage the cash flows till the property is taken possession of. But you would also end up paying higher interest for additional 2 years over and above the 20-year tenure. Considering the example above, you will pay an additional Rs.8.5 lakh interest in the 2 years during the construction phase. If the project and consequently your house possession gets delayed, the interest outgo will be much higher.

So, when should you ideally go for a pre-EMI option?

- If you have limited resources to juggle your EMIs along with your living expenses & investments and

- If you have a definite intent to sell your existing home after getting immediate possession of the new house to prepay the entire or maximum portion of the loan.

To conclude, choosing between the pre-EMI and regular EMI option will depend upon your financial situation and goals. If you are comfortable with a longer loan tenure and are willing to pay higher interest costs to ease your immediate financial burden, you should go for pre-EMIs. Also, discount the fact that some delay will be inevitable in construction projects, so you may end up paying higher interest. Ensure that the builder has a credible track record and is financially strong to complete the project within a reasonable time frame and does not cause inordinate delays.

On the other hand, if you want to minimise the overall interest cost and repay the loan over a shorter tenure, then opt for full EMIs.